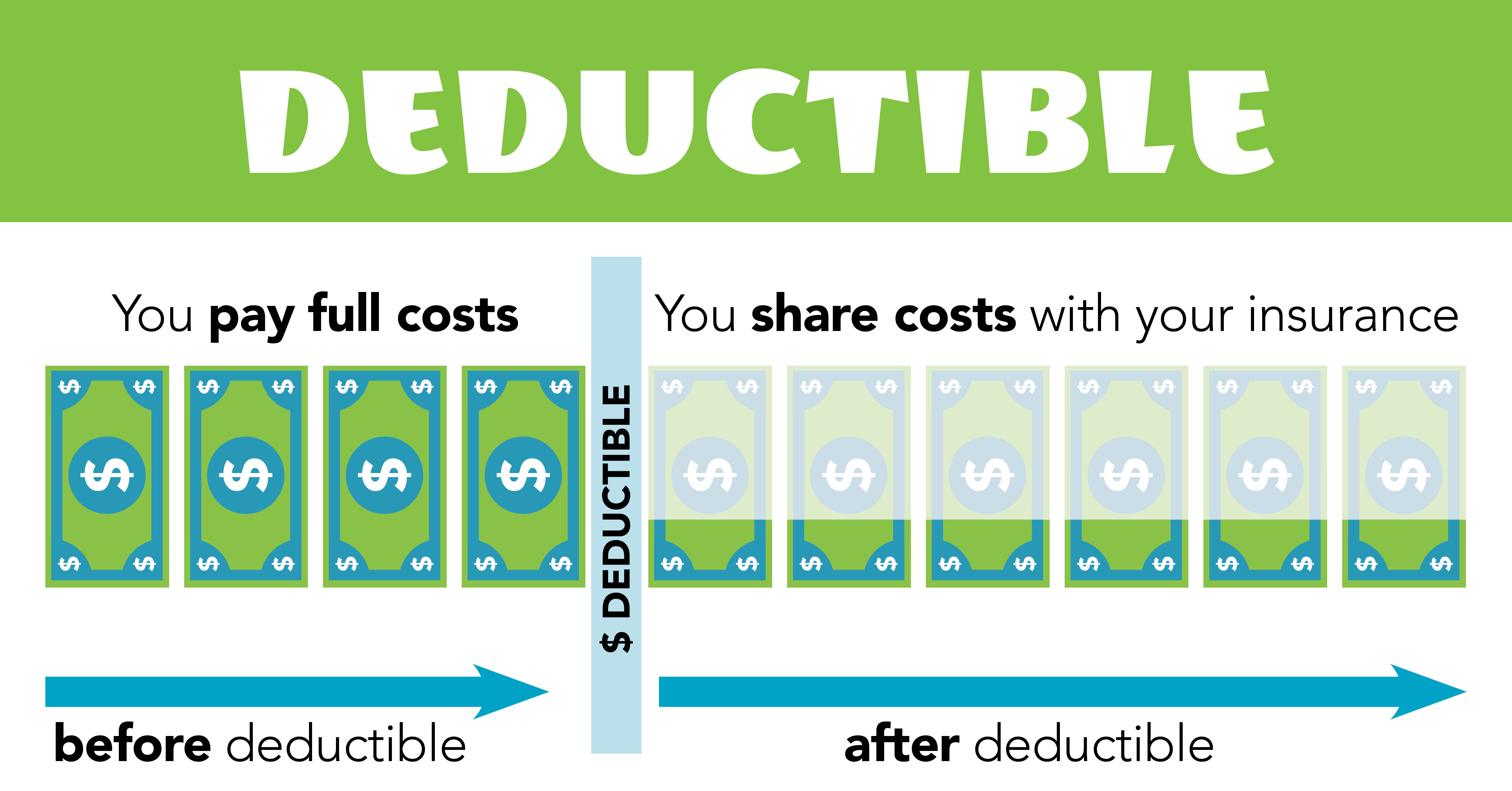

A health insurance deductible is the amount you pay out-of-pocket before your insurance covers costs. It resets annually.

Understanding health insurance deductibles is crucial for managing healthcare expenses. Deductibles can vary widely based on your insurance plan. Typically, higher deductibles mean lower monthly premiums, while lower deductibles result in higher premiums. Knowing your deductible helps you plan for potential medical costs throughout the year.

It ensures you’re financially prepared for unexpected healthcare needs. By understanding your deductible, you can make more informed decisions about your healthcare options. Always check your policy details for specific deductible amounts. This knowledge empowers you to balance your healthcare needs and financial capabilities effectively.

Credit: www.marylandhealthconnection.gov

Introduction To Health Insurance Deductibles

Understanding health insurance can be tricky. One key term is the deductible. This post will explain what a health insurance deductible is. We will also discuss why it matters to you.

Defining Deductibles

A deductible is the amount you pay out-of-pocket before insurance starts. For example, if your deductible is $1,000, you pay the first $1,000 of medical costs. After that, your insurance covers the rest.

Deductibles vary between plans. Some may be low, others high. It’s important to know your deductible amount. This helps you plan for medical expenses.

Importance Of Deductibles

Deductibles affect your overall healthcare costs. A higher deductible usually means lower monthly premiums. This can save you money if you don’t need frequent medical care.

On the other hand, a lower deductible means higher premiums. This is good if you expect many medical visits. You’ll pay less out-of-pocket each time.

Here’s a quick comparison:

| Plan Type | Deductible | Monthly Premium |

|---|---|---|

| High Deductible | $1,500 | $200 |

| Low Deductible | $500 | $400 |

Choosing the right deductible depends on your health needs. Think about how often you visit the doctor. Consider your budget for monthly payments. This helps you find the best plan for you.

Credit: www.facebook.com

How Deductibles Work

Understanding how deductibles work can save you money on health insurance. A deductible is the amount you pay before your insurance starts covering costs. Let’s dive into the details.

Annual Deductibles

An annual deductible is the amount you pay each year before your insurance kicks in. For example, if your annual deductible is $1,000, you must pay $1,000 out-of-pocket. After meeting this amount, your insurance will start to cover some or all of your medical costs.

Here’s a quick example in a table:

| Medical Expense | Amount | You Pay | Insurance Pays |

|---|---|---|---|

| Doctor Visit | $200 | $200 | $0 |

| Hospital Stay | $1,500 | $800 | $700 |

Embedded Vs. Non-embedded Deductibles

Embedded and non-embedded deductibles are important terms to know. An embedded deductible applies to each individual in a family plan. For instance, if one person meets their deductible, insurance starts covering their costs. The rest of the family still has their own deductibles to meet.

A non-embedded deductible works differently. The entire family must meet a combined deductible before insurance starts paying. Here’s a simple comparison:

| Type | How it Works |

|---|---|

| Embedded | Individual deductibles for each member |

| Non-Embedded | One combined deductible for the family |

Understanding these terms can help you choose the best health plan for your needs. Make sure to review your plan’s details carefully.

Types Of Health Insurance Plans

Understanding the types of health insurance plans is essential for making informed decisions. Different plans offer various levels of coverage and costs. Knowing these can help you choose the best plan for your needs.

High Deductible Health Plans

High Deductible Health Plans (HDHPs) have higher out-of-pocket costs. These plans usually have lower monthly premiums. HDHPs are ideal for healthy individuals who rarely need medical care. They are often paired with Health Savings Accounts (HSAs). HSAs allow you to save money tax-free for medical expenses.

- Lower monthly premiums

- Higher out-of-pocket costs

- Eligible for Health Savings Accounts (HSAs)

HDHPs are best for people who want to save on premiums. They are also suitable for those who can manage higher medical costs if needed.

Low Deductible Health Plans

Low Deductible Health Plans (LDHPs) have lower out-of-pocket costs. These plans usually come with higher monthly premiums. LDHPs are ideal for people who need frequent medical care. They provide greater financial protection in case of serious illness.

- Higher monthly premiums

- Lower out-of-pocket costs

- Better for frequent medical care

LDHPs are suitable for individuals with chronic conditions. These plans offer peace of mind with lower deductibles and predictable costs.

Impact On Healthcare Costs

A health insurance deductible can greatly affect your healthcare costs. Understanding how it works helps manage your expenses better.

Out-of-pocket Expenses

Your deductible is part of your out-of-pocket expenses. This amount must be paid before your insurance starts covering costs.

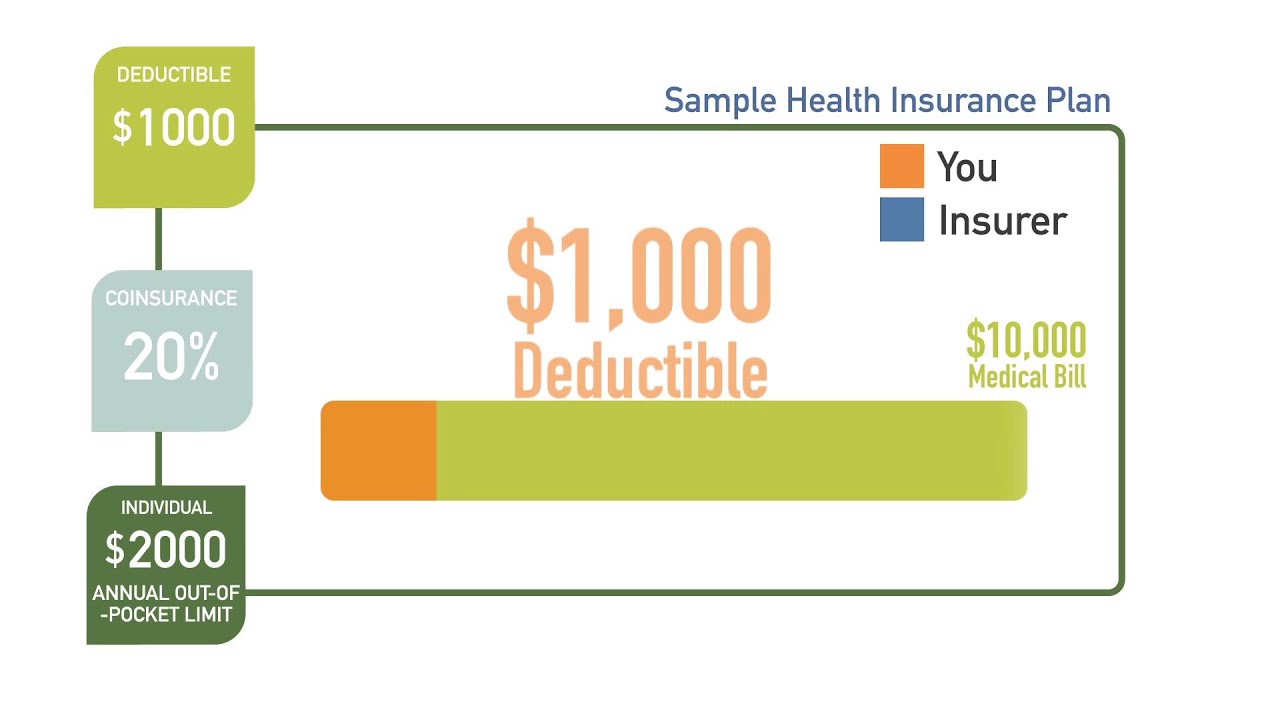

Consider the example of a $1,000 deductible. You pay the first $1,000 of your medical bills. After meeting your deductible, your insurance kicks in.

Below is a table showing how deductibles impact out-of-pocket costs:

| Deductible Amount | Out-of-Pocket Cost Before Coverage |

|---|---|

| $500 | $500 |

| $1,000 | $1,000 |

| $1,500 | $1,500 |

Copayments And Coinsurance

Besides deductibles, you also have copayments and coinsurance. These are part of your out-of-pocket expenses too.

- Copayments are fixed fees for specific services, like doctor visits.

- Coinsurance is a percentage of the cost you pay after meeting your deductible.

Here’s an example with a $1,000 deductible and 20% coinsurance:

- You pay $1,000 first.

- After that, you pay 20% of further costs.

- Your insurance covers the remaining 80%.

Understanding these terms helps you plan your healthcare budget effectively.

Choosing The Right Deductible

Deciding on the right health insurance deductible is crucial. It impacts your overall healthcare costs. Understanding your needs and financial situation helps make a wise choice.

Assessing Personal Needs

Begin by evaluating your health status. Do you visit doctors often? Have any chronic conditions? Regular doctor visits mean a lower deductible might be better.

Consider your medical history. Look at past medical expenses. These give an idea of future costs.

Family needs also matter. If you have children, they might need frequent medical attention. Think about everyone covered by the insurance.

Evaluating Financial Situation

Look at your monthly budget. How much can you comfortably spend on premiums? A lower deductible usually means higher premiums.

Consider emergency funds. Do you have savings for unexpected medical expenses? A higher deductible means paying more out-of-pocket initially.

Below is a simple table comparing different deductible options:

| Deductible Amount | Monthly Premium | Out-of-Pocket Costs |

|---|---|---|

| $500 | High | Low |

| $1000 | Medium | Medium |

| $2000 | Low | High |

Use this table to visualize the trade-offs. Balance between monthly costs and potential out-of-pocket expenses.

- High Deductible: Lower monthly premium, higher out-of-pocket costs.

- Low Deductible: Higher monthly premium, lower out-of-pocket costs.

Choose a deductible that aligns with your financial comfort and health needs.

Credit: www.youtube.com

Tips For Managing Deductibles

Understanding how to manage your health insurance deductible can save you money. Here are some practical tips to help you handle your deductibles effectively. Follow these strategies to keep your healthcare costs in check.

Budgeting For Healthcare

Start by setting aside money for healthcare expenses. Create a savings plan dedicated to medical costs. This helps cover unexpected expenses without stress. Consider setting up a separate bank account. This makes it easier to track your healthcare savings.

Use a monthly budget to allocate funds for your deductible. Calculate your estimated yearly healthcare costs. Divide this amount by 12 to get a monthly saving goal. Be consistent with your savings to stay prepared.

| Month | Amount to Save |

|---|---|

| January | $100 |

| February | $100 |

| March | $100 |

Utilizing Preventive Services

Many health plans offer free preventive services. These services do not count towards your deductible. Use these services to stay healthy and avoid costly treatments. Common preventive services include vaccinations, screenings, and annual check-ups.

Check your health plan’s list of covered preventive services. Schedule regular appointments to take advantage of these benefits. Staying proactive with your health can prevent serious issues.

- Vaccinations

- Screenings

- Annual check-ups

Utilizing preventive care can reduce your overall healthcare costs. Preventive services help catch issues early. Early detection often results in simpler, less expensive treatments.

Frequently Asked Questions

What Is A Health Insurance Deductible?

A deductible is the amount you pay before your insurance starts covering costs.

How Does A Deductible Work?

You pay out-of-pocket until the deductible is met, then insurance covers the rest.

Do All Insurance Plans Have Deductibles?

Most health insurance plans have deductibles, but the amount can vary.

Can I Choose My Deductible Amount?

Some plans allow you to choose a higher or lower deductible based on your preference.

Is A Higher Deductible Better?

A higher deductible usually means lower monthly premiums but more out-of-pocket costs upfront.

Conclusion

Understanding your health insurance deductible is essential for managing healthcare costs. It impacts how much you pay out-of-pocket. Always review your policy details to know your deductible. This knowledge helps you plan financially and make informed healthcare choices. Stay informed to maximize your health insurance benefits and avoid unexpected expenses.