If you’ve ever wondered how insurance can align with your values, especially if you seek something beyond traditional coverage, understanding Takaful insurance is key. Takaful isn’t just another insurance plan—it’s a system built on trust, cooperation, and shared responsibility.

Imagine being part of a community where everyone helps each other in times of need, and profits are returned to you rather than a company. Curious how it works and why it might be the right choice for you? Keep reading to discover the simple yet powerful principles behind Takaful insurance and how it can protect what matters most to you—ethically and fairly.

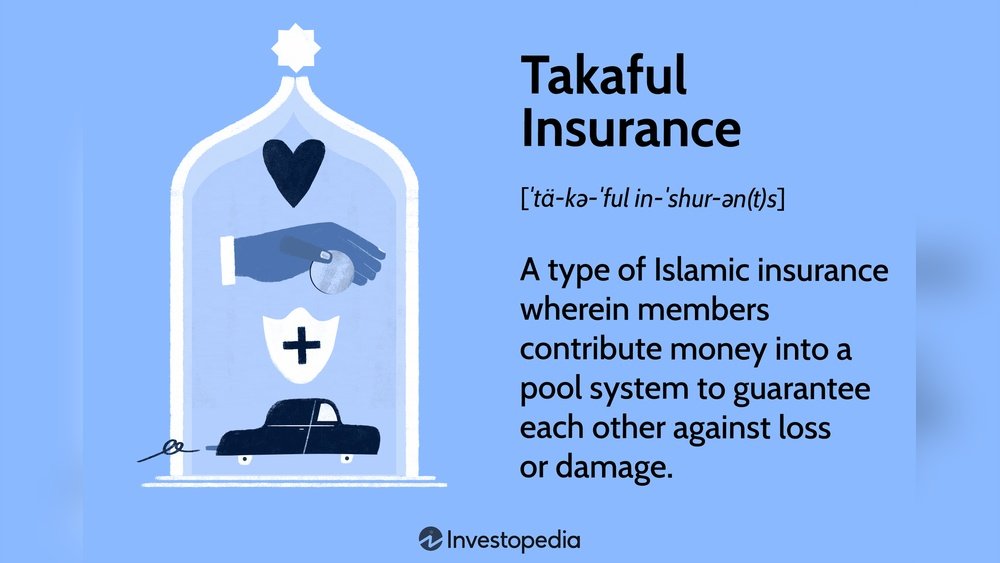

Basics Of Takaful

Takaful insurance offers a unique way to protect against risks. It follows Islamic principles and focuses on cooperation. Understanding its basics helps explain why many choose takaful over conventional insurance.

This section covers the meaning, core principles, and operation of takaful. Each part shows how takaful works in simple terms.

Meaning And Origins

Takaful means mutual guarantee in Arabic. It started from the idea of helping each other in a community. Early Muslim societies used this system to share risks and losses fairly. Today, takaful is a modern way to provide insurance that follows Islamic law.

Core Principles

Takaful is based on shared responsibility and cooperation. Participants contribute money to a common fund. This fund pays for losses faced by any member. It avoids interest and gambling, which are not allowed in Islam. Fairness and transparency are key to takaful’s success.

How It Operates

Participants agree to protect each other by pooling money. A takaful operator manages the fund but does not own it. If a member suffers a loss, the fund pays the claim. Surplus money is shared among participants or kept for future claims. This model creates a strong support system.

Credit: www.wallstreetmojo.com

Shariah Compliance

Shariah compliance is central to Takaful insurance. It ensures all operations follow Islamic law principles. This compliance builds trust among participants. It guarantees the insurance process is fair and ethical. Shariah rules prevent activities that conflict with Islamic teachings. This makes Takaful different from conventional insurance.

Prohibited Investments

Takaful funds avoid investments in forbidden industries. These include alcohol, gambling, and pork businesses. Interest-based transactions are also not allowed. The goal is to keep the fund free of riba (interest). This protects participants from unethical financial practices. The investments must align with Islamic moral values. This ensures the fund grows in a halal way.

Ethical Guidelines

Takaful follows strict ethical rules in all dealings. Transparency and honesty are key principles. Risk sharing replaces risk transfer to avoid uncertainty. The contract is based on mutual help and cooperation. Participants contribute to a common pool for protection. Profits and losses are shared fairly among them. These guidelines promote social responsibility and fairness in Takaful.

Role Of Shariah Board

The Shariah board oversees all Takaful operations. It ensures products comply with Islamic law. The board reviews contracts and investment choices regularly. Experts in Islamic finance guide the company’s decisions. They approve the Takaful model before launch. The board also audits transactions to maintain compliance. Their supervision reassures participants about the integrity of the scheme.

Risk Sharing Model

The risk sharing model is the core of Takaful insurance. It differs from conventional insurance by focusing on cooperation. Participants work together to protect each other from financial loss. This system builds trust and fairness among everyone involved.

Mutual Guarantee Concept

In Takaful, participants agree to guarantee one another. This means each person supports the group. If a member faces a loss, others help cover the cost. This mutual promise creates a strong community bond. It reduces the burden on any single individual.

Pooling Of Funds

Participants contribute money to a shared fund. This pool is used to pay claims. The contributions are based on the risk each member carries. The fund grows as more people join. This collective saving ensures enough money is available for those in need.

Profit And Loss Distribution

Any profits made from the fund are shared among participants. Losses are also shared fairly within the group. This system avoids unfair gains or losses. It keeps the process transparent and just for everyone. Participants benefit directly from the fund’s performance.

Types Of Takaful

Takaful insurance offers different types tailored to various needs. Each type follows Islamic principles, promoting cooperation and shared responsibility. Understanding these types helps in choosing the right Takaful plan for personal or business protection.

Family Takaful

Family Takaful focuses on long-term financial protection. It covers life risks and provides savings benefits. Participants contribute to a common fund for mutual support. It helps families secure their future and manage financial risks.

General Takaful

General Takaful covers non-life risks like property, vehicles, and businesses. It protects against damage, theft, and other losses. Participants share the risk and contribute to the fund. This type supports everyday needs and business continuity.

Health And Medical Takaful

Health and Medical Takaful offers coverage for medical expenses. It helps with hospital bills, treatments, and surgeries. Participants contribute to a shared pool that pays claims. This type ensures access to healthcare without financial strain.

Benefits Of Takaful

Takaful insurance offers many unique benefits. It combines financial protection with ethical values. Participants share risks and rewards together. This system builds trust and mutual help. It suits people seeking fair and transparent insurance solutions.

Ethical And Transparent

Takaful follows clear Islamic principles. It avoids interest and gambling elements. Every transaction is open for participants to see. This honesty creates confidence in the system. People know their money is handled fairly.

Community Support

Participants work as a community. They help each other in times of need. Contributions go into a shared fund. Losses are covered by this collective pool. This support network strengthens social bonds.

Financial Security

Takaful provides reliable financial protection. It covers accidents, health, and property risks. Claims are paid from the common fund. This ensures timely help for members. It gives peace of mind against uncertainties.

Credit: www.youtube.com

Takaful Vs Conventional Insurance

Takaful and conventional insurance both protect against risks. They differ in principles and operations. Understanding these differences helps you choose the best option.

Both systems offer financial security. The key lies in how risk, investment, and profits are handled.

Risk Transfer Vs Risk Sharing

Conventional insurance works on risk transfer. You pay premiums to shift risk to the insurer. The insurer bears the loss if it occurs.

Takaful uses risk sharing. Participants contribute to a common pool. Losses are paid from this pool, shared among all members.

This creates a sense of mutual help and cooperation. Everyone supports each other in times of need.

Investment Differences

Conventional insurance invests premiums freely for profit. Investments may include interest-based products.

Takaful invests funds following Islamic law. It avoids interest (riba) and unethical businesses. Investments focus on halal (permissible) ventures only.

This ensures the funds grow in a Shariah-compliant way, respecting ethical guidelines.

Profit Handling

Conventional insurers keep all profits. Policyholders do not share in the gains.

Takaful profits belong to the participants. Surplus funds are shared or returned after expenses.

This system builds trust and fairness. Participants benefit from good performance of the fund.

Eligibility And Accessibility

Takaful insurance offers an alternative to conventional insurance, based on cooperation and shared responsibility. Understanding who can participate and where it is available helps clarify its eligibility and accessibility. This section explores the key aspects that determine access to Takaful insurance plans.

Who Can Participate

Anyone willing to join the Takaful scheme can participate. Participants contribute to a common fund. This fund is used to help those who face a loss. The system promotes mutual support among members. No strict restrictions limit participation based on age or profession. Eligibility mainly depends on the willingness to follow Takaful principles.

Non-muslim Participation

Takaful is based on Islamic principles but not exclusive to Muslims. Non-Muslims can join and benefit from Takaful plans. The ethical nature of Takaful appeals to many people. It avoids interest and uncertainty, which some find attractive. The inclusive approach encourages wider participation beyond religious boundaries.

Global Availability

Takaful insurance is expanding worldwide. It is popular in countries with large Muslim populations. Many regions in Asia, the Middle East, and Africa offer Takaful products. Some Western countries also provide access to Takaful plans. Growth in global markets improves accessibility for more people. Online platforms make it easier to join from different locations.

Choosing A Takaful Plan

Choosing the right Takaful plan requires careful thought. It ensures you get the coverage you need while following Islamic principles. This section helps you understand the key steps in selecting a plan that fits your situation and budget.

Assessing Needs

Start by identifying what you want to protect. Consider your family’s financial needs and future goals. Think about health, education, and emergency expenses. Clear needs guide your choice of coverage and sum assured. Avoid buying unnecessary benefits that increase costs.

Comparing Providers

Not all Takaful providers offer the same services. Check their reputation and customer reviews. Look for companies with clear policies and good support. Compare the coverage options, claim process, and financial strength. Choose a provider that suits your trust and comfort level.

Understanding Terms And Fees

Read the plan’s terms carefully. Know what is covered and what is excluded. Pay attention to fees, charges, and contribution amounts. Understand how the surplus is shared among participants. Clear knowledge of terms avoids surprises and helps you make an informed decision.

Challenges And Future Trends

The Takaful insurance sector faces several challenges as it grows globally. Understanding these challenges helps in predicting future trends. The industry must adapt to market demands, regulatory frameworks, and technological changes. These factors will shape the future of Takaful insurance.

Market Growth

Takaful insurance shows steady growth in many regions. Rising awareness about Shariah-compliant products drives new participants. However, competition with conventional insurance remains strong. Expanding into new markets requires educating people about Takaful’s unique benefits. Small market size in some areas limits growth potential. Creating trust among customers is crucial for broader acceptance.

Regulatory Issues

Regulations differ widely across countries offering Takaful products. Some rules do not fully support Islamic insurance principles. Lack of clear guidelines creates uncertainty for providers and clients. Harmonizing regulations would help Takaful companies operate smoothly. Compliance with both Islamic law and local laws is complex. Regulators must balance consumer protection with industry growth.

Technological Innovations

Technology offers new ways to improve Takaful services. Digital platforms make enrollment and claims processing faster. Mobile apps increase accessibility for remote users. Blockchain can ensure transparency and trust in fund management. Artificial intelligence helps assess risks and detect fraud. Adopting these technologies boosts efficiency and customer satisfaction.

Credit: insurancebegins.com

Frequently Asked Questions

What’s The Difference Between Insurance And Takaful?

Insurance transfers financial risk to a company through premiums. Takaful involves participants pooling funds to mutually share and cover losses ethically.

Is Takaful Only For Muslims?

Takaful is based on mutual cooperation and ethical principles. It is open to everyone, not just Muslims. Non-Muslims can also participate and benefit from takaful plans.

What Is The Basic Concept Of Takaful?

Takaful is a cooperative insurance where participants contribute to a shared fund. They mutually guarantee protection against losses, following Islamic principles. The fund covers claims, and any surplus returns to participants. It emphasizes risk-sharing, ethical investments, and community support without interest or uncertainty.

What Are The Benefits Of Takaful?

Takaful offers ethical, Shariah-compliant protection by sharing risks among participants. It promotes mutual support, transparency, and profit sharing. It avoids interest and uncertainty, ensuring fair and cooperative financial coverage for all members.

Conclusion

Takaful insurance offers a clear, ethical way to protect against risks. It relies on shared responsibility among participants. This system avoids interest and uncertainty, following Islamic principles. People contribute to a common fund to help those in need. Profits are shared fairly, not kept by companies.

Many find takaful suits their values and needs. Understanding takaful helps in choosing the right protection. It provides peace of mind with a community focus. Consider takaful as a trustworthy option for insurance coverage.